FBAR for US Expats in the Netherlands (2026): Verified Filing Guide

Source-verified FBAR guide for Americans in NL: $10,000 aggregate threshold, filing route, deadlines, Form 8938 interaction, and current virtual-currency status.

Who This Applies To

This page is for U.S. persons (for example U.S. citizens, green-card holders, and certain entities) living in the Netherlands who hold or can control foreign financial accounts.

IRS FBAR guidance states the filing obligation is under the Bank Secrecy Act and reported on FinCEN Form 114.

The $10,000 Aggregate Test

IRS states FBAR filing is required when the aggregate value of foreign financial accounts exceeds $10,000 at any time during the year.

- It is not a per-account threshold.

- Financial interest and signature/other authority can both trigger reporting.

- IRS also states taxable-income generation is irrelevant for FBAR reportability.

Practical implication: do annual account maximum tracking, not just year-end balance tracking.

Which Accounts Usually Matter in NL

IRS examples include bank, brokerage, and similar foreign financial accounts. In practice for NL-based expats, this usually means reviewing all non-U.S. banking and investment relationships each year.

Ownership is not the only trigger: signature authority can matter under IRS FBAR rules.

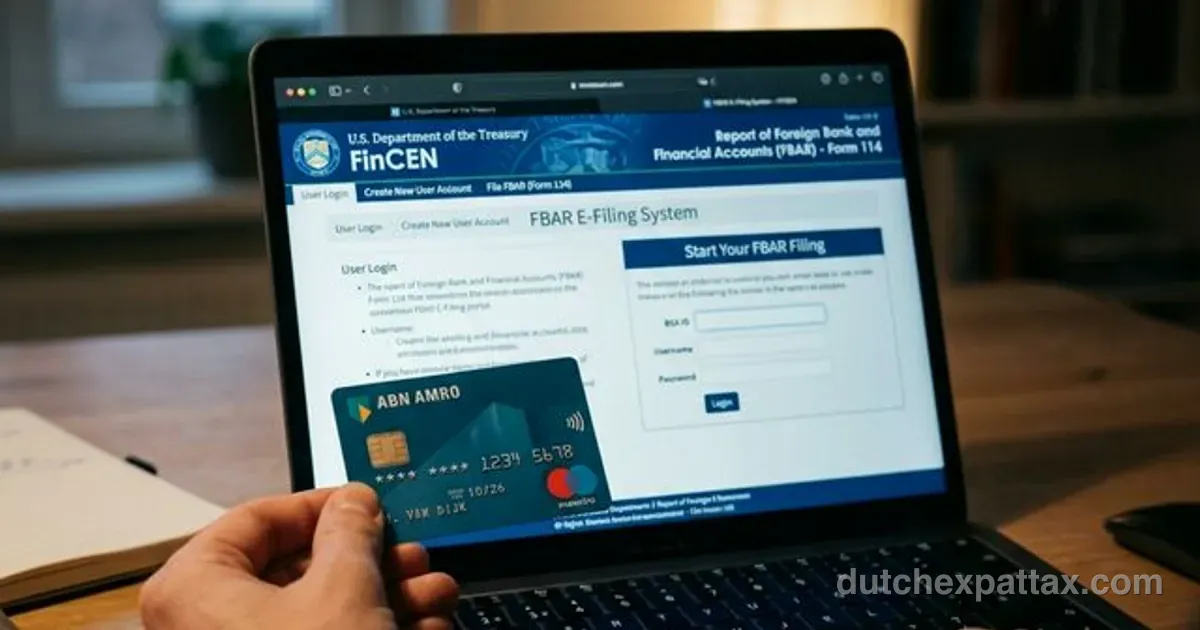

How and When to File FBAR

- Collect maximum annual values for each reportable foreign account.

- Prepare account holder, account number, institution name/address, and account type records.

- File electronically via FinCEN BSA E-Filing (NoReg FBAR filing route is available).

IRS states FBAR due date is April 15 and provides an automatic extension to October 15.

IRS also states recordkeeping is generally required for 5 years from the FBAR due date.

FBAR vs Form 8938

FBAR and FATCA Form 8938 are separate regimes. The IRS Form 8938 instructions show different threshold frameworks and residency/filing-status tests.

| Item | FBAR (FinCEN 114) | Form 8938 |

|---|---|---|

| Filed with | FinCEN BSA E-Filing | IRS return package |

| Core trigger style | $10,000 aggregate foreign-account test | Thresholds vary by filing status and residency tests |

| Can both apply? | Yes | Yes |

For U.S. taxpayers living abroad, Instructions for Form 8938 provide threshold tables and definitions (including the 330-day/presence abroad context).

Virtual Currency Status (Current Rule)

FinCEN Notice 2020-2 states that, at the time of that notice, a foreign account holding only virtual currency was not yet defined as a reportable FBAR account, while FinCEN indicated intent to propose amendments.

Treat this as an area to re-check each filing season against current FinCEN and IRS guidance.

Late Filing and Penalty Reality

IRS states late or non-filing can trigger civil and/or criminal consequences, with civil maximums adjusted annually for inflation.

If you are delinquent and not under IRS civil/criminal investigation, IRS guidance says to file late FBARs as soon as possible and follow FinCEN instructions for late-filing explanations.

Official Sources

- IRS: Report of Foreign Bank and Financial Accounts (FBAR)

- FinCEN BSA E-Filing: NoReg FBAR filing route

- FinCEN: FBAR information portal

- IRS: About Form 8938

- IRS: Instructions for Form 8938 (threshold framework)

- FinCEN Notice 2020-2: virtual currency reporting status

- Federal Register: inflation adjustments for civil monetary penalties

- U.S. Supreme Court: Bittner v. United States (2023)

FAQ

Do I need FBAR if I had brief balance spikes only?

Potentially yes. IRS uses the "at any time during the year" aggregate test.

Can I paper-file FBAR?

IRS says e-filing is required unless FinCEN grants a specific paper-filing exemption.

What if I missed prior years?

IRS guidance points to delinquent FBAR filing instructions. File promptly and document your reason as required by that process.

Does FBAR itself create extra U.S. income tax?

FBAR is a reporting regime. Income tax treatment is handled separately under U.S. tax return rules.